|

The best part about being in the start-up community is watching other start-ups. Almost every week, I learn about a new company that stops me in my tracks and makes me say, “Damn, that is so obvious. ABC company is going to forever change the way we do XYZ.” Here are three companies that have given me this reaction.

Kickstarter Venture capital was created 56 years ago. Before Eugene Kleiner’s shot-in-the-dark letter that landed on Arthur Rock’s desk, there was no institution for funding smart people with new ideas. That changed when Rock connected Kleiner and 7 other colleagues with Sherman Fairchild. Fairchild invested $1.5 million into the 8 transistor scientists to create Fairchild Semiconductor. Fairchild Semi was a success, at first, but soon the founders left because they did have enough equity. Two Fairchild employees - Robert Noyce and Gordon Moore - went on to found Intel. (To learn more about the fascinating history of VC and The Valley, check out this interview and the movie Something Ventured.) Venture capital was a tectonic innovation in finance. But in the last half century, not much has change: VCs raise money from Limited Partners and invest in young, un-established companies with mountains of potential. In fact, the major innovation has been the rise of secondary markets like SharesPost and SecondMarket. These exchanges give shareholders of private companies liquidity, which is great. But these markets have not changed the fundamental way in which early stage ideas get funded. The way that VC offered equity financing for early stage companies, Kickstarter offers working capital finance. This is huge. Before Kickstarter, working capital finance was restricted to established companies that had good relationships with banks. Now, a company with a novel product idea can create a Kickstarter campaign and pre-sell units. Since the company receives the money before shipping the product, they have capital on hand to deliver the promised product. In short, Kickstarter gives early stage entities a form of finance that did not previously exist for them. The key question is will Kickstarter launch a billion dollar business? Naysayers say no way; Kickstarter is for crafts and movies. I say, if Kickstarter was around in 1976, Jobs and Wozniak would have created the “Apple 1” campaign. TalkTo Look at the data. Texting is on the rise; voice calling is on the decline. Recognizing this, TalkTo created an app that allows anyone to text any question to any business. Want to know if Whole Foods has your favorite microbrew? Launch TalkTo, select Whole Foods, and shoot off a text. Running late for a dinner reservation? No worries; TalkTo has your back. I was in New York City this weekend and used TalkTo half a dozen times. It worked flawlessly. I was able to get a restaurant reservation, change said reservation, and double check that we would be seated outside. Within one day, TalkTo inserted itself between me and every business that I interact with. In other words, TalkTo -- not the restaurant, bank or hotel -- owns the relationship. This is incredibly powerful: owning the customer relationship is the holy grail in business. In the insurance industry, for example, brokers and underwriters constantly struggle to own the policyholder relationship. Owning the relationship enables companies to better understand customer needs and ensure quality interactions, leading to customers that stay longer and buy more. By building a simple app that delivers as promised, TalkTo is poised to change the way that people find information about and interact with companies. What company recently did that? I’ll give you a hint. It starts with a “G” and ends with an “oogle.” GigWalk I love services that create marketplaces. The two most recent examples are Airbnb and Uber. Airbnb looked at the world and said how can we connect supply (people with spare beds) with demand (people looking for an inexpensive place to stay). Uber did the same thing, connecting underutilized Town Cars with people seeking reliable and convenient car services. GigWalk is connecting businesses that need market research with people looking to make a few dollars. A brand - think Colgate, P&G, etc - needs to understand (or audit) how its products are being placed on the shelf at retailers. The brand could send in a dedicated “secret shopper,” which is costly and logistically challenging. Or, the brand could use GigWalk to push an alert to anyone in the area and ask them to simply take a photo of the Dental Section. I particularly like GigWalk because it is an everyday product. A simple trip the grocery store or Starbucks or a restaurant could net a GigWalker a few dollars. In short, GigWalk looked at the world and said how can we use existing tools to mobilize people to solve a business challenge.

11 Comments

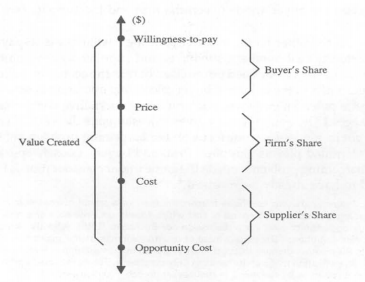

Today, is a “turning point” day. Yesterday, Spottah went live on the Apple app store. For more than two years, I have wanted to play the mobile game, so yesterday was an enormous milestone. Tomorrow, I will receive my diploma from New York University’s Stern School of Business. For three years, I attended Stern at night while working during the day. So as I close one chapter and open another, I want to take a moment to share my most memorable lessons from Stern's classrooms. The goal of the MBA is to teach students frameworks in which to tackle real world problems. We covered a ton of frameworks but here are my three favorites. The Value Chain It is easy to grasp that profits rise when you increase revenue and reduce costs. But what does that actually look like in an interconnected supply chain? Enter the The Value-Based Business Strategy by Adam Brandenburger and Harborne W. Stuart, Jr. Every firm sits in the middle of the value chain at some point. The firm buys resources from suppliers (raw materials, labor), turns those resources into a higher-value product, then sells that product to a buyer. Let’s use a clothing company, for example. The company buys fabric from a supplier and hirers workers. Inside the firm, workers turn raw fabric into fabulous garments. The firm then sells those garments at a higher cost to a retail store. In the diagram below, this transaction is marked by the “cost” and the “price.” Pretty straight forward. Here is where the value-based strategy comes into play. The total value of the chain is the buyer’s willingess-to-pay MINUS the supplier’s opportunity cost. The goal of a company is to capture as much of the value chain as possible. This means pushing the cost of inputs downwards to the supplier’s opportunity cost, i.e. the point right before it makes sense for the supplier to walk away and not make the sale. The same thing goes on the buyer side. The goal of the firm is to push upwards the price of its goods to the buyer’s willingness-to-pay. Vibram soles and Intel chips are great examples. Traditionally, these two products were commodities; no one cared about the sole of their shoe or the chip in their computer. As a result, the bootmakers and computer manufacturers captured the lion share of the value in the chain, i.e. there was a big spread between the price charged by Vibram/Intel and willingness-to-pay of Asolo/Dell. So what did Vibram and Intel do? They branded the components. Vibram advertised and put the bright yellow marker on each of its soles. Intel advertised, too, most famously creating the “Intel Inside” campaign. Customers soon demanded the yellow brand on their soles and wanted to know if Intel was inside their PC. This shifted the value away from the end manufacturer and towards the component maker, thus allowing Vibram and Intel to push towards the buyer’s willingness-to-pay point.

The Value Chain (courtesy of Professors Brandenberg and Stuart and the Journal of Economics & Management Strategy)

The Value Formula

Sticking to value, but this time we’re are talking my favorite topic: Finance. Whenever new information arises and I’m trying to value an asset (stock, bond, property, you name it), I rely on a piece of advice from my valuation professor. “When new information comes to light ask yourself: what lever of the ‘value’ formula is being affected?” More specifically, the professor was referring to the perpetuity discounted cash flow (DCF) formula, which is: Value = Cash Flow / (Cost of Capital - Growth Rate of Cash Flows). The levers are the cash flows generated by the asset, the growth rate of those cash flows, and the opportunity cost of capital, i.e. the minimum return acceptable to investors. The purpose of the formula is to discount future cash flows into a net present value. The formula is not perfect, mainly because it assumes constant growth in cash flows, but it is an excellent rule of thumb. To put this in perspective, let’s say you own stock in a Company X. News breaks that the company lost a major contract. What lever is being affected? Cash flow; the company will generate less cash than before. One could also argue that cost of capital is at risk of rising, assuming a reduction in cash flows reduces the company’s chance of survival and thus increases the risk level. But the main lever being pulled is cash flow. Let’s put some numbers to this. Assume before the news, total cash flows were $100, cost of capital was 10% and growth was 3%. Thus, the asset is worth $1,428 (100 / (10%-3%)). Having lost the contract, cash flows are estimated to fall to $75, which causes the value of the company to fall to $1,071 ($75 / (10%-3%)). This is super simple finance but it a great framework to understand quickly how certain events affect asset prices. In short, always ask “what lever is being pulled: cash, cost of capital, growth?” The Growth Diamond So far, the frameworks have been very quant-ey -- my apologies. So let me finish strong with a framework taught by Robert Wright that explains why some countries develop rapidly, like the United States, while others do not develop at all. It comes down to the “Growth Diamond;” Stern professors notoriously love baseball. Home plate is a non-predatory, Lockean government. In other words, growth starts with a government that protects the life, liberty and property of its citizens. Such a government collects taxes transparently, regularly and at a reasonable rate. The government also establishes and enforces reasonable laws. Note that such a government does not need to be a democracy; though they often are. The next phase of development, or first base, is a financial system in which capital moves from savers to borrowers. First base cannot be reached without home plate; after all, the crux of saving and lending are contracts recognized by the courts established by the government. With home plate and first base established, the economy is prepared to take second base: entrepreneurship. Individual actors are comfortable investing into a long-term business knowing that the government will not pilfer it in the night. And even if something goes wrong, the actor has faith that the slip of paper called “insurance” will be made good. And lastly, the actor has access to capital, thanks to first base. Interestingly, not all economies move equally between bases. There are countries with non-predatory governments and financial systems that have less entrepreneurship than others. The final stage, third base, is a management system. Basically, the entrepreneurs that flourished from a stable government and access to capital eventually grow into large, distributed organizations. These organizations have the systems required to undertake large and complex markets like air travel, chip fabrication and automobile manufacturing. I find this framework incredibly helpful as I look at emerging markets. The first question is what type of government does the country in question have? If the answer is non-predatory, than you can begin to look down the base path. The growth diamond is also good for understanding domestic policy. I find myself asking how will a new law or regulation effect any of the bases. In closing, the MBA education was amazing. As I think about more frameworks and lessons, I will do my best to share. Several years ago, I negotiated my first term sheet with an angel investor. At the time, I was raising money for a company I founded with Brent Ridge -- yes, the same Brent from “The Fabulous Beekman Boys”. We were fresh-faced students and first-time entrepreneurs negotiating with a first-time angel. Neither of us knew what we were doing, so the negotiation devolved into who could swing the biggest one. No shocker here: the deal fell through and our company was not funded. During the negotiation, I remember thinking, “Why isn’t there a framework to at least start the conversation about the deal terms?” Anything was better than just throwing outrageous numbers on the wall to see what stuck. Well, after years of experience and studying, I have learned that there is a framework for evaluating early stage deals - in fact, there are two. I have built models for both frameworks and made them available as a Google Template; also available at the bottom of this post. If you’re an early stage investor, these models will help you evaluate deals. And if you’re an entrepreneur, they will help you understand how investors should be thinking about your opportunity. As you use these tools, please remember they are not valuating your company. Rather, these frameworks evaluate the deal. In industry-speak, the tools test “finance-ability” And one last thing: Please note, only change the YELLOW cells. The VC Method The first framework is called The VC Method, which is well documented by Andrew Metrick and Ayako Yasuda. The VC Method compares the present value (PV) of a future exit with the current investment. If the PV of an exit is greater than the current investment, than invest. If it is smaller, than walk away. Let’s look at an example. The deal on the table is as follows: $250,000 for 33% of the company. Ok, that is pretty straightforward. Now, put on your thinking caps. To understand the PV of an exit we need to know (i) the potential size of an exit, (ii) the probability chance of the exit occurring, (iii) the number of years until said exit, (iv) how much dilution will occur between today and the exit and, finally, (v) the VC cost of capital. Ok, that is a lot. Where to begin? Exit size is obviously the biggest “what-if.” Could you have called $23B for a search engine in 1998? Probably not. So pick a reasonable number based on the market you’re entering and then adjust with a probability chance of success. For this illustration, let’s assume a 50% chance of a $10M exit. Again, the exit size and the probability chance of the exit depends on the market opportunity, strength of the team, economic conditions -- and the list goes on. Get familiar with these factors and populate the model as you like. The next three factors are a bit easier. Time to exit refers to how long the investment will be locked away. It could be as little as one year or ten-plus years. Three to five years is a good middle ground. Retention is a measurement of dilution; more specifically, it is the stake in the company at the time of exit as a percent of the original stake. And lastly, the VC Cost of capital is the discount rate. This refers to the cost of capital on the entire VC portfolio and not this single investment. Why? Because risk was already factored in when we assigned a probability chance to the exit. Thus, the average VC is looking for a 15-20% return. This can change as market conditions change; for example, if interest rates climb, than VC cost of capital will, too. Alright, that’s a lot of info, so let’s go back to the template. The template is pre-populated with assumptions that our $250,000 investment in exchange for 33% of the company has a 50% chance of exiting for $10M in 3 years. We also assumed significant dilution (50%) and a 15% cost of capital. Drum roll, please....Under those assumptions, it is a good investment because the expect return is $547k, which is greater than the initial $250,000 invested. Play around with the numbers and see what you get. For example, if you lower the probability chance of a $10M exit to 20%, which is reasonable, the deal becomes unfavorable. Or, if everything is held constant constant except it takes 3-times as long to exit (9 years), then the deal becomes unfavorable. What percent is the correct percent In the above method, we assume that the deal is structured: $250k for 33% of the company, take it or leave it. Well, this is often not the case. What often happens is the company is looking for a certain amount of capital and the investor needs to decide what amount of equity they need in return. The second model on the tab entitled “% of company required” calculates the minimum equity stake required for a particular deal. This model is taught by Alexander Ljungqvist of NYU Stern. If the investor gets less equity than model calculates, than they will not achieve the target rate of return -- a bad thing. But if the investor gets more, than it is all gravy. This is a much more straight forward model, so let’s dive in. The first variable is simple: How much is the company asking for? In this illustration, let’s assume $1M. In terms of dilution, it is an early stage deal so let’s assume 50%. Now we get to the exit, which is more difficult indeed. Again, the size and timing of an exit depends on the market opportunity, the team, the company’s competitive advantage, plus hundreds of other factors. Take all these factors into consideration and come up with a reasonable best case scenario. For this example, I assume a $25M exit in 5 years. Ok, last part: the investor’s target rate of return. In the previous model, we used the return on the portfolio and represented risk with the probability chance of an exit. In this model, we simply use the target rate of return for this one investment. Thus, the return is greater to reflect the risk of this investment and because of the need to supplement other investments that will be dogs. A rate as low as 25% to as high as 60% is acceptable. For this model, I assume 45%. So without further adieu, a $1M investment in a company that gets diluted by 50% and exits in 5 years for $25M requires an equity stake 38.46%, assuming a 45% target return. Again, play around with the numbers. For example, by lowering the exit size to $20M but moving the exit up 1 year, the required stake falls to 33.15%. Lastly, I have built another tool that allows you to see what the return will be for a given equity stake. For example, if instead of getting 38.46% of the company you get 10%, the investor’s return will be 10.76%. This is well below the target rate of return and thus unacceptable. |

JONATHAN STEIMAN

I'm the Founder and CEO of Peak Support. This blog is my take on early-stage companies and innovation. Every so often, there may be a post about culture, networking, family -- you name it. After all, what is a blog if it isn't a tad bit unstructured.

Archives

December 2016

Categories

All

|